(1) The US has limited capacity to finance a soft landing given the size of the public deficit, the extent of household indebtedness. He`d have to lift taxes or print money to offer any largesse. Given the amount of money slushing around the US economy, the US is not weak, even in the wake of Hurricane Katrina, 10 consecutive rises in the Fed rate and higher oil prices. But the US has to fund its largesse, and the spirit of the US consumer will change as oil prices bight and inflation takes off. The US government can only respond by printing money, and this will cast doubt upon foreign government's strategy of buying US treasuries. With rising inflation, we can expect more Asian governments to shift to gold, not to mention individual investors. Expect a bright picture for gold.

(2) The US cant rely on a strong terms of trade like Australia to support equities & incomes when the property market comes off. Mind you the Australian market has further to fall, as all markets will fall with the collapse of the US market. Asian savings are unlikely to be spent on consumption given the surplus export capacity in those markets, and their fiscal conservatism. The US has accounted for 75% of global financing demands...thats not an easy vacuum to fill.

Rises in commodity prices are impressive, but look outside those markets which are easily traded with derivatives, eg. look aside from those COMEX & LME traded commodities to contract-based markets like iron ore, coal, tantalum, zircon. That`s where you will get a better idea of market fundamentals. Mind you most of the speculative money has gone into copper because its the most liquid commodity market. Next will be gold!!!

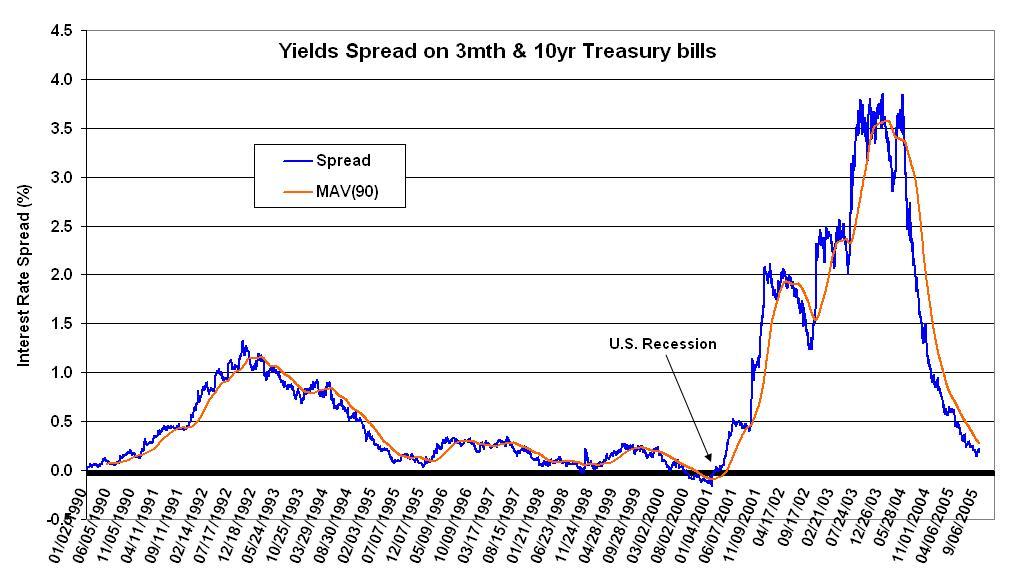

The following charts shows the state of the bond market. The first chart shows the interest rate differential or 'spread' between the long market bond rates and the shorter term rates, which are strongly influenced by the Fed-set rate. When the differential is small, there is little incentive for the short-term refinancing. When the differential goes negative, banks have no benefit from lending funds short term because they can get better long rates. This severely undermines economic activity leading to recession. The impact is particularly bad when interest rates are high, but regardless the impact is not positive given that rates appear to be on the rise and households are so heavily indebted.

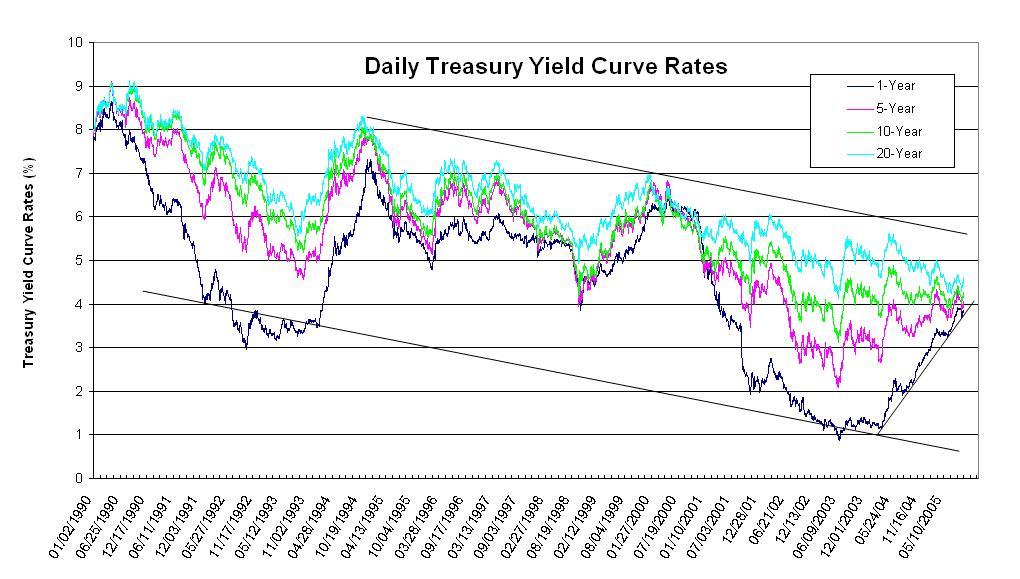

The 2nd chart shows the differences between the various US treasury debt securities based on their maturity. Its apparent that there is a strong correlation between term rates. Its evident that the Fed has resorted to strong monetary stimulus to kickstart the US economy after the US internet-tech wreckage of 2000, when it drove the Fed rate well below market rates. From the chart its apparent that this is not the first time that the Fed (under Greenspan) has resorted to such stimulus. Perhaps that was the rationale for Greenspan's easy monetary policy - 'It worked last time, might it work again'. Well consider that the stimulus at the time resulted in the internet bubble, and that we are now at a more mature stage of the economic cycle.

Doesn't the downward trend in interest rates however suggest that we are still on an expansionist trend. I would suggest that is the appearance by virtue of monetary stimulus. Macroeconomic factors to me suggest that this cannot go on as long as Asian savings are channelled into the US market and mis-applied on household largesse.

The question is whether the US Federal Reserve will continue to lift the Fed rate to keep ahead of inflationary expectations. The answer is - It has no choice. But inflation can't be fought by lifting rates. That just curtails further lending and spending. There is still too much money sloshing around, and it can only be counter-acted by productive investment or the liquidation of loans. This requires a collapse of the housing market or debt repayments. Thats an unlikely trend given that the US savings rate is back below 1%. Expect a collapse in the US housing market like the collapse in the Dow/Nasdaq in 2000-1. Greenspan or his replacement might be inclined to ignore inflation and reduce rates, but its unlikely because Asian governments won't fund the US economy. They will be buying gold to counter their $US exposure. Since their export markets will be collapsing, and they will face domestic challenges stimulating domestic demand at home with infrastructure projects, expect them to start liquidating some of their US bond holdings. Expect a run on the $US, driving the $US to historic lows. Sadly there will be no export markets for the US to service given the over-capacity in the global marketplace. It will likely take about 3-4 years for the global economy to work through the excess capacity. The US government cannot expect to finance the malaise given its fiscal position and its reliance on Asian (45% holdings) treasury holdings. It will have to raise taxes and interest rates will also have to be higher.

No comments:

Post a Comment